USD 33.2 billion. That's the size of the global payment security market in 2025, and it is projected to reach nearly USD 91.6 billion by 2032 while helping protect an estimated $37.45 trillion in digital transaction value by 2026, according to Maximize Market Research on the global payment security market.

That number matters because it changes the framing. Payment security isn't an IT side task. It's the control system behind revenue collection, customer trust, compliance, and dispute prevention. If your business accepts tuition payments, telemedicine fees, subscription renewals, webinar registrations, or invoice settlements, your payment flow is part of your core operation.

Small and mid-sized businesses often make one costly mistake. They assume attackers only care about banks or large marketplaces. In practice, smaller organizations are attractive because they often mix customer service, payment handling, video calls, chat, and email into one workflow without clearly securing each handoff. A clinic may take bookings on a website, send payment links in chat, discuss billing on video, and store records in a separate system. Every step is a security boundary.

Why Payment Security Is Your Business Lifeline

Payment security is the combination of technology, process, and access control that protects card data, payment credentials, and transaction integrity. It covers more than the checkout page. It includes who can view customer details, how payment data moves through your systems, how you verify users, and how quickly you can detect abuse.

For an ed-tech company, weak payment security means failed renewals, refund disputes, parent complaints, and a damaged brand. For a telemedicine provider, it can also create privacy exposure around billing conversations and patient records. The practical consequence isn't abstract. Revenue gets delayed, staff time gets pulled into cleanup, and customers start asking whether they should trust you with the next payment.

What businesses often get wrong

Many teams still treat payment security like a compliance folder. They collect policies, complete a questionnaire, and assume the job is done. That approach fails because real payment abuse happens inside daily operations.

Common examples include:

- Shared admin access: Multiple staff members use the same login for payment or meeting tools, so nobody can trace who changed what.

- Uncontrolled payment links: Teams send links over email, SMS, chat, and live sessions without consistent verification.

- Too much data exposure: Customer service or billing staff can see more payment information than they need.

- Disconnected tools: Video meetings, CRM records, reminders, and payment processing run in silos, which creates blind spots.

Practical rule: If a customer can pay you through more than one channel, you need to secure more than one channel.

Trust is a revenue asset

Customers rarely compliment a secure payment flow. They notice when it feels normal, quick, and safe. They definitely notice when it feels suspicious. A confusing authentication prompt, a fake-looking payment request, or an unprotected webinar link can push a legitimate buyer away just as effectively as fraud can.

Strong payment security does three things at once. It reduces the chance of fraud, lowers your compliance burden when designed properly, and makes your business easier to trust. That's why it belongs in operational planning, not just in a security policy.

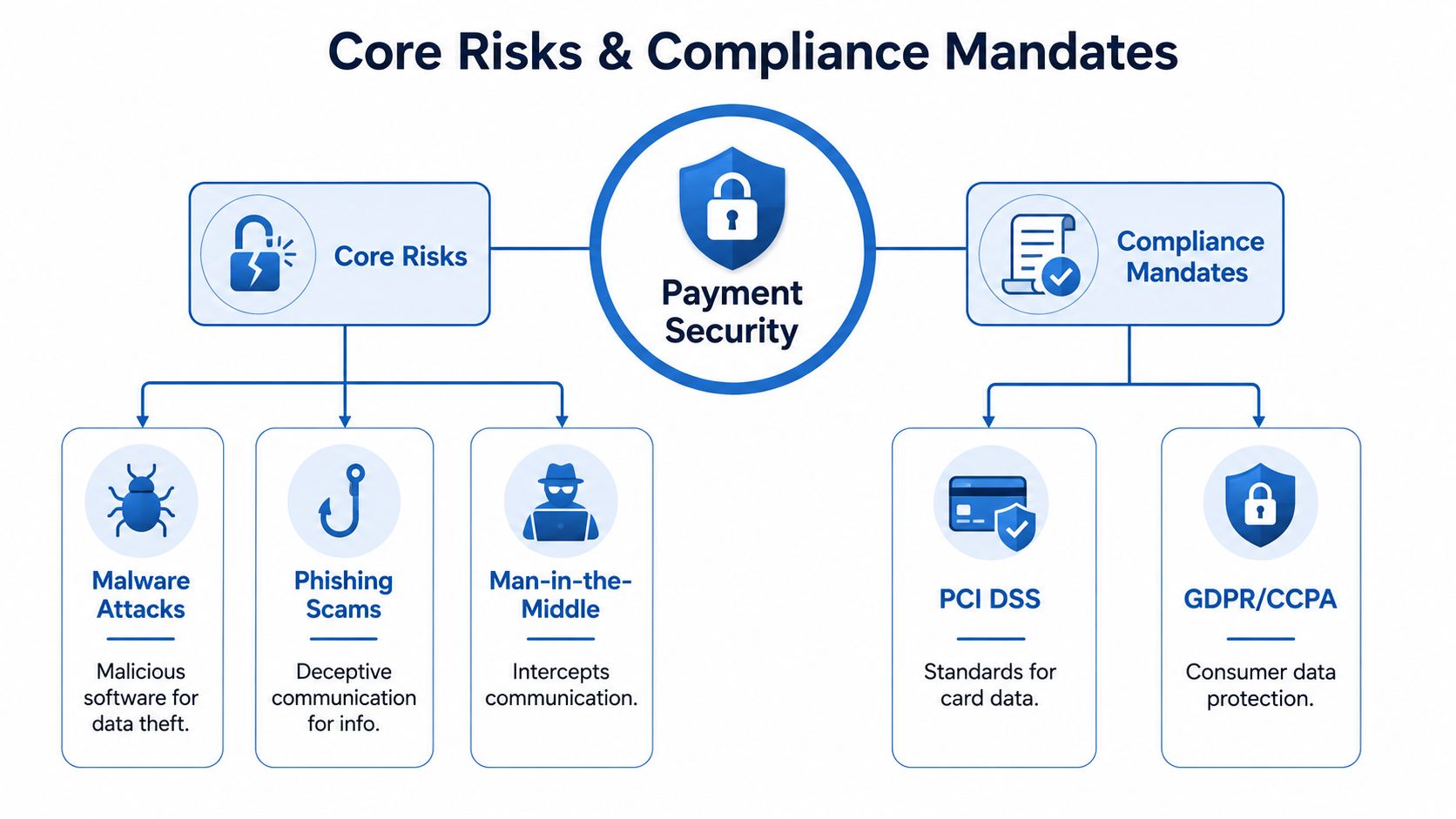

Understanding Core Risks and Compliance Mandates

Payment attacks don't always look dramatic. Most start with ordinary business communication. A fake invoice approval email. A staff member tricked into sharing credentials. A payment link sent through a chat thread that no one verifies. By the time finance notices the issue, the damage has already moved into refunds, unauthorized charges, and customer complaints.

The risks that hit SMBs most often

Phishing is still one of the easiest ways into a payment environment. An attacker doesn't need to break your encryption if they can trick a staff member into handing over access.

Malware can capture credentials, monitor devices, or scrape sensitive information from poorly secured systems. If billing staff use unmanaged endpoints or mix personal and business activity on the same device, risk goes up fast.

Man-in-the-middle attacks target the path between user and service. That matters when customers or staff interact with payment pages, admin panels, or shared links over untrusted networks.

For contact-heavy businesses, the blind spot is usually non-web channels. Payment conversations happen over phone, SMS, chat, and support desks, not just at checkout. That's why teams responsible for omnichannel support should study practices around data protection in contact centers, especially when agents send links, verify identities, or discuss account changes.

Compliance has changed from periodic to continuous

PCI DSS isn't just a standard for large retailers. If your business stores, processes, or transmits cardholder data, it affects you. The practical value of PCI DSS is simple. It forces discipline around encryption, access control, monitoring, and system hardening.

The bigger change is in how businesses need to operate. The shift to continuous, risk-based compliance under PCI DSS 4.0.1 replaces the old annual checkbox mindset. As of April 2025, mandatory controls such as CVV encryption during authorization and remote-access PAN copying prevention require ongoing intelligence-driven processes, not just a yearly audit, according to Cyber Defense Magazine's review of digital payment security trends and realities of 2025.

That has a direct operational meaning for SMBs:

- Annual audits won't catch daily drift: Staff permissions change, tools get added, workflows expand, and exceptions creep in.

- Remote support creates hidden exposure: Temporary admin access, screen sharing, and copied payment details can inadvertently break policy.

- Monitoring becomes part of compliance: You need evidence that controls continue to work, not just that they existed during an assessment window.

Compliance that only works during audit week doesn't work.

HIPAA and payment handling in healthcare

Healthcare providers sometimes separate HIPAA from payments too aggressively. Billing, teleconsultation, intake, reminders, and payment collection often overlap in the same workflow. If staff discuss balances during appointments, share links during virtual sessions, or manage patient communication in one platform and billing in another, privacy and payment security need to be aligned.

A useful starting point is to review how your meeting and workflow stack supports data protection and compliance for regulated communication. The key isn't just secure storage. It's controlling how payment-related information is viewed, shared, and acted on across the whole customer or patient journey.

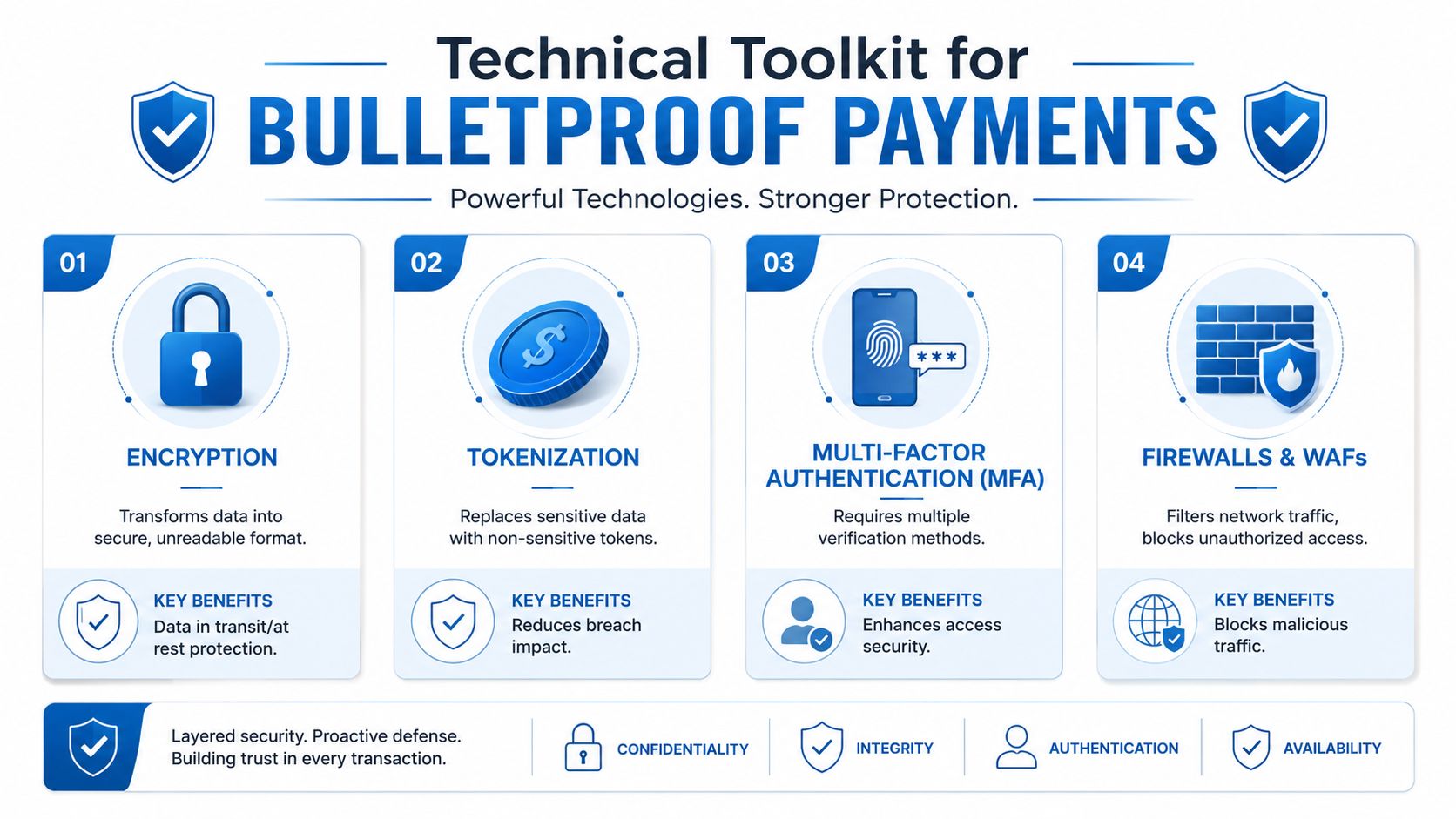

Your Technical Toolkit for Bulletproof Payments

Technology solves payment risk only when each control has a clear job. Too many businesses buy overlapping tools and still leave obvious gaps. The better approach is to build a tight stack where every layer handles a different part of the problem.

Encryption protects data in motion and storage

Encryption is your sealed digital envelope. If someone intercepts the contents, they still can't read them without the key. In practical payment environments, that starts with TLS 1.3 encryption with AES-256 cipher suites, which forms the baseline for protecting payment data in transit and at rest. Organizations that combine end-to-end encryption, tokenization, and MFA achieve higher PCI DSS compliance rates, which directly correlates with reduced fraud incidents, according to HighRadius on payment security fundamentals.

That doesn't mean every encryption setup is equal. What works:

- Strong transport encryption: Use modern protocols for all payment-related sessions.

- Secure key management: Encryption without disciplined key handling is weaker than it looks.

- Coverage across workflows: Apply protection not only on checkout pages but also on admin access, APIs, logs, and recordings where applicable.

What doesn't work is assuming a firewall alone is enough. Firewalls are traffic control. They are not a substitute for encrypted data handling.

A related control worth understanding is end-to-end encryption in browser-based communication. It matters when payment discussions, support interactions, or webinar-based selling happen inside live sessions rather than only on a website.

Tokenization reduces the blast radius

If encryption is a sealed envelope, tokenization is a casino chip. It stands in for value, but it isn't the true value. Sensitive payment data, such as the primary account number, gets replaced with a non-sensitive token. The merchant uses the token, while the original data sits in a secure vault outside the merchant's environment.

That changes the risk profile in a useful way. A stolen token is generally useless to an attacker without access to the underlying vault and the controls around it. It also helps reduce PCI scope because your systems handle less raw card data.

Stripe's payment security guidance notes that providers using tokenization report a 60 to 70 percent reduction in data breach impacts compared with relying on encryption alone, as summarized in Stripe's overview of payment security and tokenization.

Here's where businesses benefit most:

| Control | Business effect | Why it matters |

|---|---|---|

| Tokenized card data | Less sensitive data in your systems | Smaller target for attackers |

| Vaulted storage | Payment credentials handled outside your app | Lower operational burden |

| Reduced data exposure | Fewer teams see raw payment details | Easier access governance |

Field advice: If your staff can do their job without seeing the full card data, your system should be designed that way.

MFA, gateways, and scope reduction

Multi-factor authentication is the lock on the room around your payment tools. It doesn't protect card data directly. It protects the accounts that can touch customer records, refunds, gateway settings, and reporting dashboards.

MFA matters most for:

- Admin panels for payment processors

- CRM systems tied to billing actions

- Support tools that can resend payment links or update customer details

- Meeting and webinar platforms where hosts control attendee access and shared content

Then there's the payment gateway. Think of it as an armored truck. Instead of dragging sensitive data through your own application stack, you hand the risky part to a specialist designed to transport and process it securely.

The final concept is PCI scope reduction. This is one of the most practical ideas in payment security. The fewer systems, people, and workflows that touch real payment data, the fewer things you need to defend, monitor, document, and audit. Businesses that ignore scope reduction usually end up with expensive security sprawl and fragile compliance.

Active Defense with Fraud Detection and Monitoring

Even a well-built payment stack will miss fraud if nobody watches what happens after deployment. Fraudsters adapt faster than documentation does. They test weak refund rules, compromised accounts, unusual login times, and support channels where staff are under pressure to move quickly.

Monitoring catches what static controls miss

A static control says, “This user has access.” Monitoring asks, “Does this behavior make sense right now?”

That distinction matters. A real-time detection system can flag behavior such as a customer account logging in from an unusual context, a burst of failed payment attempts, repeated refund requests, or a host sharing payment instructions in an unexpected session workflow. Modern systems often use machine learning and behavior analysis for risk scoring in real time, which is also part of how 3D Secure can block suspicious transactions before authorization in the payment flow, as described in the earlier tokenization discussion.

What active defense looks like in practice

For most SMBs, active defense doesn't need a giant security operations center. It needs disciplined review and clear response paths.

Use this baseline:

- Real-time alerts: Route urgent signals to the people who can act, not just to a generic inbox.

- Log reviews: Check admin changes, failed authentication attempts, link creation, refunds, and permission changes.

- Exception handling: Require a second review for unusual payment actions such as high-risk refunds or account changes.

- Channel awareness: Watch support desks, chat, and phone-based workflows, not just web checkout.

One area businesses underestimate is the connection between fraud prevention and post-transaction operations. If you also need stronger processes for fighting payment disputes, bring fraud signals and dispute evidence together. The same logs that help you catch suspicious behavior early can help you answer chargebacks later.

The fastest way to lose money twice is to miss the fraud first and fail the dispute second.

A connected customer workflow also helps. If your communication, reminders, and customer records live in separate places, staff often miss patterns that would have looked obvious in one view. That's why teams benefit from tighter coordination across CRM and email marketing workflows, especially when payment reminders, support communication, and account verification intersect.

Secure Payments in Practice with AONMeetings

The easiest way to understand secure payment operations is to look at where SMBs collect money. Not every payment starts on a storefront. Many happen around live interactions such as consultations, demos, paid webinars, training sessions, or parent counseling calls.

For those businesses, the meeting platform itself becomes part of the payment security picture.

A paid webinar example

An educator runs a paid exam-prep webinar and shares access details with registered attendees. The risky version of this workflow is common. A reusable meeting ID gets forwarded, a payment link appears in a public chat, and late joiners enter without review.

A more secure setup uses waiting rooms, password-protected meeting IDs generated uniquely for each session, and moderator controls that lock meetings after all attendees join. These controls prevent unauthorized access to payment links and session content during live product launches and training events, which aligns with the webinar and meeting security practices described by Perivan's video conferencing security best practices.

That value proposition is practical, not theoretical. The host controls who gets in, when the room closes, and who can share content. That sharply reduces the chance that a non-paying attendee receives the same billing or access path as a legitimate customer.

A telemedicine billing example

A clinic schedules follow-up consultations and collects fees around virtual appointments. In this setting, encryption as an added feature matters because billing discussions, patient identity checks, file sharing, and appointment records can overlap inside one session.

Bank-level encryption with AES-256 for data in transit and at rest is a strong baseline for video-assisted billing workflows, especially when staff also use MFA and strong passwords before joining sensitive meetings, as discussed in Slack's guidance on secure video conferencing. If the platform also supports end-to-end encryption by default across call types, with keys generated locally on participant devices rather than transmitted to the provider, it adds another layer of protection during screen sharing and file exchange, as outlined in Wire's explanation of encrypted video conferencing.

For clinics and regulated service providers, those details matter because payment security isn't limited to the payment page. It extends to the communication environment around the transaction.

Price comparison and business value

SMBs often assume secure platforms are automatically too expensive. That's not always true. Enterprise-grade video conferencing platforms with built-in payment security and HIPAA compliance such as AONMeetings start at ₹179 per user per month, while traditional enterprise platforms with similar security can exceed ₹1,500 per user monthly, making the secure option up to 8.5x more cost-effective, according to CSIS analysis on video conferencing technology and risk.

Here's the practical comparison.

| Feature | AONMeetings | Traditional Enterprise Platform |

|---|---|---|

| Starting price per user per month | ₹179 | Can exceed ₹1,500 |

| HIPAA-compliant setup | Included in platform positioning | Often available, usually at higher cost |

| Webinars included | Included | Often limited, add-on, or bundled at higher tiers |

| Encryption as an added feature | Bank-level encryption included | Commonly available, but often tied to higher-cost plans |

| Waiting rooms and moderator controls | Included | Usually available |

| Auditor-ready compliance logs | Included in the value proposition | Often positioned as enterprise functionality |

The value proposition goes beyond price. You get webinars included, which matters for educators, trainers, clinics running awareness sessions, and product teams doing paid launches. You also avoid the usual problem of stitching together one tool for meetings, another for webinars, and another for compliance tracking.

That consolidation has security value. Fewer moving parts usually means fewer weak handoffs.

Building Your Simple Payment Security Roadmap

If you run a small or mid-sized business, don't try to secure everything at once. Start with the payment paths that already exist. Most organizations know their website checkout. They forget the payment links sent by support, the billing details discussed on calls, the webinar registrations, and the manual overrides in admin tools.

Start with a channel inventory

List every place a customer can pay, confirm a payment, ask for a refund, or receive billing instructions. Include:

- Web checkout

- Phone and chat support

- SMS or email payment links

- Video meetings and webinars

- Back-office billing tools

You're looking for where sensitive data appears and who can access it.

Reduce exposure before adding complexity

Your next move should be architectural, not cosmetic.

- Choose third-party tools that keep raw payment data out of your own environment where possible.

- Turn on encryption, MFA, and role-based access across payment-adjacent systems.

- Use tokenization through your payment provider so staff and internal apps don't handle more sensitive data than necessary.

- Shrink PCI scope by limiting which systems and employees can interact with payment details.

Train the people in the workflow

The biggest gaps often sit between tools. Staff need to know how to verify requests, when not to resend a payment link, how to handle screen sharing safely, and which channels are approved for billing communication.

Good payment security depends on ordinary habits done consistently.

Review access regularly. Check logs. Treat payment operations as a living process, not a compliance file. That's what keeps revenue flowing and customer trust intact.

If you want a simpler way to support secure meetings, webinars, and regulated communication without enterprise-level pricing, take a look at AONMeetings. It's built for Indian organizations that need browser-based collaboration, webinars included, strong encryption, and compliance-friendly workflows in one platform.